Falling four days in a row, China’s main stock index, the Shanghai Composite, has plummeted below the 3,000 threshold. This represents a huge loss of money for the investors involved. But it’s worth remembering that the stock market remains relatively peripheral to the wider Chinese economy. Indeed, China’s “Black Monday” is more a product of the wider economic concerns the country faces, than it will be a trigger for any kind of economic collapse.

China has two stock exchanges that were established in the early 1990s. Together, they rank second in the world in terms of market capitalisation (the total money market value of the shares being traded), just after the New York Stock Exchange. In terms of the trading volume on the Chinese market, it is four times larger than on the NYSE, with about 3% of the market value being traded every day.

The Shanghai and Shenzhen stock exchanges were established as part of China’s economic reform process. Their initial purpose was to assist the reform and privatisation of China’s vast state-owned enterprises. It was hoped that they would evolve to form a critical component in the country’s financial system, promoting a more efficient allocation of financial resources. But this has not been the case. Accompanied by frequent government interventions and largely closed to foreign investors, China’s stock markets remain highly inefficient.

A volatile market

Unlike Western stock exchanges where institutional investors take the leading role, over 80% of the participants in the Chinese stock market are individual investors. Instead of viewing stock market investment as a long-term investment, they tend to bet on speculative returns. This has directly led to big boom and bust cycles.

Since the last stock market bubble of 2006-07, Chinese stock markets remained gloomy for about seven years until mid-way through 2014 – as shown in the graph above. The resurgence in stock market activity was a result of government regulators increasing the amount of credit available to individual investors. It also coincided with a contraction in the real estate market, which had formerly been the main investment option for individuals.

The lack of correlation between China’s stock market performance and the country’s economic performance exemplifies its peripheral nature to the wider economy. When the market crashed in October 2007 (before the credit crunch had a serious impact on the world financial system), economic growth in China remained steady. Similarly, China’s stock market upsurged before the recent crash, despite the country’s economic growth declining to a decade-low level. The rollercoaster ride of the stock market is therefore much more closely related to the speculative behaviour of investors – not the wider economy.

Government action

When the stock market began to plummet earlier this July, the Chinese government reacted quickly and decisively, implementing a full pack of rescue measures to stabilise the market. These ranged from direct share purchase to the investigation of any illegal behaviours of the people involved. It spent 5 trillion RMB (US$800 billion or the equivalent of almost 10% of China’s GDP in 2014) in its reserve, to prop up its wobbly stock markets.

But the impact of this huge rescue effort did not achieve the desired outcome. After recovering gradually by about 1,000 points, the market collapsed again, seemingly after disappointing data suggesting further slowing in China’s industrial activity and by the failure of the Chinese government to unveil bold enough market interventions to prop up equity prices.

In many ways the crash has been a correction that better reflects the value of Chinese stocks. But a mood of panic entered the market. Fears over China’s slowing economy were accompanied by a lack of confidence in the ability of the Chinese authorities to prop up the market.

Now the government has implemented the measures that were previously expected. The People’s Bank of China (the country’s central bank) has cut interest rates and promised to pump more liquidity into the banking sector. We can expect the stock market to stop dropping as a result and edge back to a level that is closer to its true value (around 3,500-4,000 points).

The need for strong government intervention raises serious concerns about China’s plan to further liberalise its financial system to bring in greater competition and to turn the country’s currency, RMB, into an international currency. It is clear that China’s attempts to reform itself towards a full market-based economy has come to a critical stage and the government will be extremely cautious about further steps forward. Nevertheless, it was lucky that unlike the US or UK where a large population is exposed to the market, China’s stock markets have little connection with its real economy and play a much smaller role in its economic development.

This article was originally published on The Conversation.

China has two stock exchanges that were established in the early 1990s. Together, they rank second in the world in terms of market capitalisation (the total money market value of the shares being traded), just after the New York Stock Exchange. In terms of the trading volume on the Chinese market, it is four times larger than on the NYSE, with about 3% of the market value being traded every day.

The Shanghai and Shenzhen stock exchanges were established as part of China’s economic reform process. Their initial purpose was to assist the reform and privatisation of China’s vast state-owned enterprises. It was hoped that they would evolve to form a critical component in the country’s financial system, promoting a more efficient allocation of financial resources. But this has not been the case. Accompanied by frequent government interventions and largely closed to foreign investors, China’s stock markets remain highly inefficient.

A volatile market

Unlike Western stock exchanges where institutional investors take the leading role, over 80% of the participants in the Chinese stock market are individual investors. Instead of viewing stock market investment as a long-term investment, they tend to bet on speculative returns. This has directly led to big boom and bust cycles.

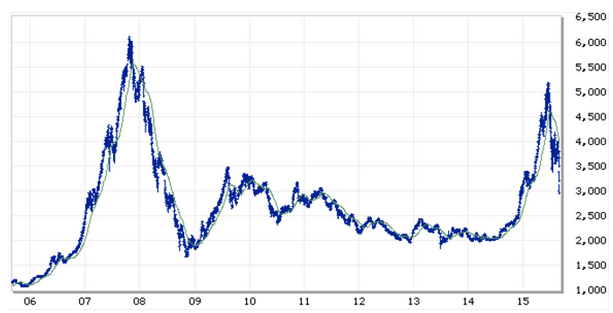

Boom and bust cycles: China’s benchmark stock index, the Shanghai Composite from 2006. MarketWatch

Since the last stock market bubble of 2006-07, Chinese stock markets remained gloomy for about seven years until mid-way through 2014 – as shown in the graph above. The resurgence in stock market activity was a result of government regulators increasing the amount of credit available to individual investors. It also coincided with a contraction in the real estate market, which had formerly been the main investment option for individuals.

The lack of correlation between China’s stock market performance and the country’s economic performance exemplifies its peripheral nature to the wider economy. When the market crashed in October 2007 (before the credit crunch had a serious impact on the world financial system), economic growth in China remained steady. Similarly, China’s stock market upsurged before the recent crash, despite the country’s economic growth declining to a decade-low level. The rollercoaster ride of the stock market is therefore much more closely related to the speculative behaviour of investors – not the wider economy.

Government action

When the stock market began to plummet earlier this July, the Chinese government reacted quickly and decisively, implementing a full pack of rescue measures to stabilise the market. These ranged from direct share purchase to the investigation of any illegal behaviours of the people involved. It spent 5 trillion RMB (US$800 billion or the equivalent of almost 10% of China’s GDP in 2014) in its reserve, to prop up its wobbly stock markets.

But the impact of this huge rescue effort did not achieve the desired outcome. After recovering gradually by about 1,000 points, the market collapsed again, seemingly after disappointing data suggesting further slowing in China’s industrial activity and by the failure of the Chinese government to unveil bold enough market interventions to prop up equity prices.

In many ways the crash has been a correction that better reflects the value of Chinese stocks. But a mood of panic entered the market. Fears over China’s slowing economy were accompanied by a lack of confidence in the ability of the Chinese authorities to prop up the market.

Now the government has implemented the measures that were previously expected. The People’s Bank of China (the country’s central bank) has cut interest rates and promised to pump more liquidity into the banking sector. We can expect the stock market to stop dropping as a result and edge back to a level that is closer to its true value (around 3,500-4,000 points).

The need for strong government intervention raises serious concerns about China’s plan to further liberalise its financial system to bring in greater competition and to turn the country’s currency, RMB, into an international currency. It is clear that China’s attempts to reform itself towards a full market-based economy has come to a critical stage and the government will be extremely cautious about further steps forward. Nevertheless, it was lucky that unlike the US or UK where a large population is exposed to the market, China’s stock markets have little connection with its real economy and play a much smaller role in its economic development.

This article was originally published on The Conversation.

You’ve read Scroll.

Now help sustain it

Scroll is funded by readers, not corporate owners. If you believe our work matters, support our newsroom. Become a member today!

We’re not driven by clicks or corporate interests – just honest, independent reporting. Keep us going. Support Scroll today!