It is well established that Prime Minister Narendra Modi’s Jan Dhan Yojana has a serious problem. The financial inclusion scheme has achieved its objective of opening 10 crore bank accounts by January, but more than 70% of those have no money in them. The problem is more severe among private sector banks, where the sums deposited in Jan Dhan accounts are really meagre.

According to the Finance Ministry’s data, only 30% of all accounts opened in private banks under the Jan Dhan Yojana have money in them.

The Ministry of Finance claims that it has provided access to financial services to 98.4% of India's households and is now tackling the challenge of making these accounts active.

“We will deliberate on how to keep the accounts active,” Hasmukh Adhia, secretary, department of financial services, told the Business Standard. “We will also have to see how to use these accounts for DBT [direct benefit transfers], pension distribution and other benefits.”

Five major private sector banks – ICICI, Kotak Mahindra, Yes Bank, IndusInd Bank and Karur Vaisya Bank – have opened nearly nine lakh Jan Dhan accounts thus far, but the aggregate deposit in them is just a little over Rs 1,000. Four of the banks have next to no money in their accounts.

It is estimated that of the 29 lakh accounts opened so far under the scheme in a total of 15 private sector banks, about 20 lakh are lying dormant, with zero balance.

Public sector banks, too, have their laggards: State Bank of Mysore and State Bank of India have a dormancy rate of almost 95%. On the whole, though, public sector banks have performed better. Eighteen such banks have managed to keep the tally of dormant accounts below the national average of 72%.

In State Bank of Travancore, for instance, just 14% of the Jan Dhan accounts have no balance. In five others, including Bhartiya Mahila Bank and Canara Bank, the proportion of dormant accounts is 50%.

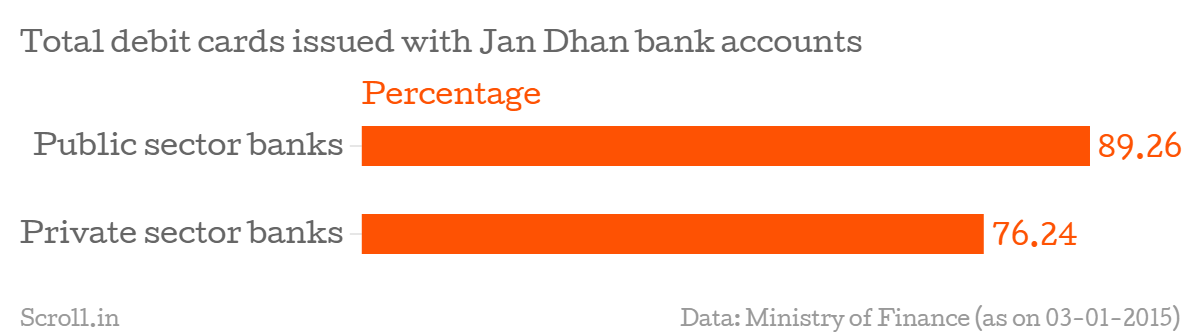

In issuing the promised debit cards too, public banks have done better, as evident from the above chart. They have provided cards to more than 88% of the account holders. In contrast, private banks are a step behind, distributing debit cards to over 76% account holders.

According to the Finance Ministry’s data, only 30% of all accounts opened in private banks under the Jan Dhan Yojana have money in them.

The Ministry of Finance claims that it has provided access to financial services to 98.4% of India's households and is now tackling the challenge of making these accounts active.

“We will deliberate on how to keep the accounts active,” Hasmukh Adhia, secretary, department of financial services, told the Business Standard. “We will also have to see how to use these accounts for DBT [direct benefit transfers], pension distribution and other benefits.”

Five major private sector banks – ICICI, Kotak Mahindra, Yes Bank, IndusInd Bank and Karur Vaisya Bank – have opened nearly nine lakh Jan Dhan accounts thus far, but the aggregate deposit in them is just a little over Rs 1,000. Four of the banks have next to no money in their accounts.

It is estimated that of the 29 lakh accounts opened so far under the scheme in a total of 15 private sector banks, about 20 lakh are lying dormant, with zero balance.

Public sector banks, too, have their laggards: State Bank of Mysore and State Bank of India have a dormancy rate of almost 95%. On the whole, though, public sector banks have performed better. Eighteen such banks have managed to keep the tally of dormant accounts below the national average of 72%.

In State Bank of Travancore, for instance, just 14% of the Jan Dhan accounts have no balance. In five others, including Bhartiya Mahila Bank and Canara Bank, the proportion of dormant accounts is 50%.

In issuing the promised debit cards too, public banks have done better, as evident from the above chart. They have provided cards to more than 88% of the account holders. In contrast, private banks are a step behind, distributing debit cards to over 76% account holders.

You’ve read Scroll.

Now help sustain it

Scroll is funded by readers, not corporate owners. If you believe our work matters, support our newsroom. Become a member today!

We’re not driven by clicks or corporate interests – just honest, independent reporting. Keep us going. Support Scroll today!